Perpetual inventory has been seen as the wave of the future for many years. It has grown since the 1970s alongside the development of affordable personal computers. These UPC codes identify specific products but are not specific to the particular batch of goods that were produced. This more specific information allows better control, greater accountability, increased efficiency, and overall quality monitoring of goods in inventory. The technology advancements that are available for perpetual inventory systems make it nearly impossible for businesses to choose periodic inventory and forego the competitive advantages that the technology offers.

Your Financial Accounting tutor

- The technology advancements that are available for perpetual inventory systems make it nearly impossible for businesses to choose periodic inventory and forego the competitive advantages that the technology offers.

- In this lesson, I explain the easiest way to calculate inventory value using the LIFO Method based on both periodic and perpetual systems.

- This section will discuss some of the most common situations where implementing a perpetual inventory system can be highly beneficial.

- For example, Ava wants to figure out the average cost to assign for Acetone repackaged in her company’s warehouse.

- Since businesses often carry products in the thousands, performing a physical count can be difficult and time-consuming.

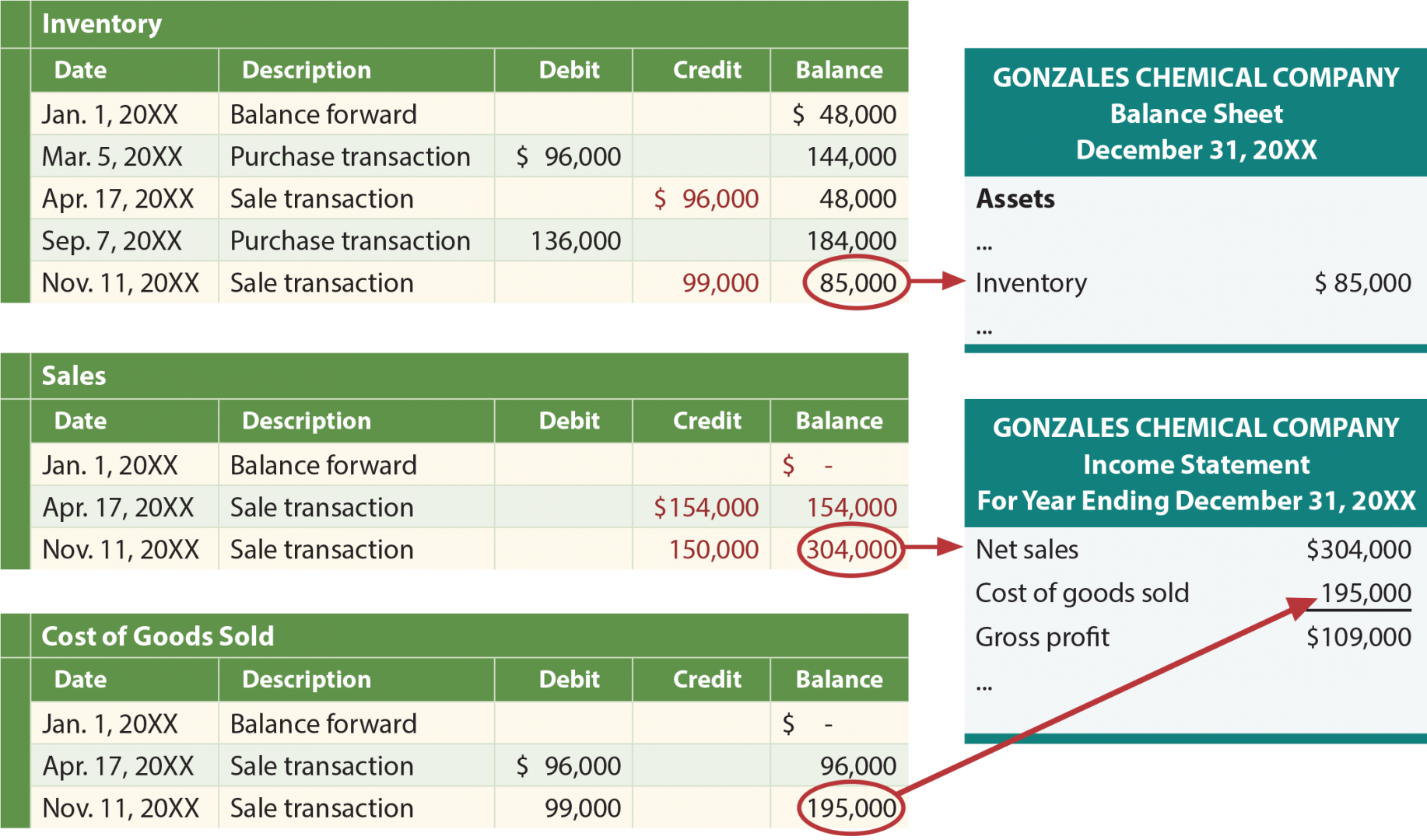

- You can use WAC to calculate an average unit cost, COGS for a period and ending inventory for a period.

Assume our physical inventory count reveals 80 units in ending inventory. Hence, the cost of ending inventory is $192, composed of four units in beginning inventory (4 units x $38 each) and one unit from purchases (1 x $40 each). The four paddles present at the beginning of the period at $38 each are still included in inventory at the end of the period. This is because the most recent paddles purchased were assigned to Cost of Goods Sold under the LIFO inventory method. Figure 10.18 shows the gross margin resulting from the LIFO perpetual cost allocations of $7,380.

Example – LIFO periodic system in a manufacturing company:

A company can still assign costs to ending inventory assuming the four paddles are still physically in the inventory. ABC International acquires 10 green widgets on January 15 for $5, and acquires another 10 green widgets at the end of the month for $7. Under a perpetual LIFO system, you would charge the cost of the five widgets sold on January 16 to the cost of goods sold as soon as the sale occurs, which means that the cost of goods sold is $25 (5 units x $5 each). The costing results of a perpetual LIFO system are more common than a periodic net working capital definition LIFO system, since most inventory is now tracked using computerized systems that maintain inventory records on a real-time basis. For example, the inventory balance on January 3 shows one unit of $500 that was purchased first at the top, and the remaining 22 units costing $600 each that were later acquired shown separately below. If the inventory units sold during a day are equal or less than the inventory units purchased during the same day, we will assign that day’s cost to the inventory sold because it is the most recent purchase cost.

Improve Inventory Management with FreshBooks

The periodic inventory system requires a physical count of inventory at the end of the period. Most companies using periodic inventory systems are small businesses that only count inventory and calculate COGS once per year. However, if you want to use the periodic inventory system monthly, you can estimate the units in ending inventory without taking a physical count. The last-in, first-out (LIFO) method is one of the three inventory cost flow assumptions, alongside the FIFO (first-in, first-out) and average cost methods. It’s only permitted in the United States and assumes that the most recent items placed into your inventory are the first items sold.

Using the FIFO inventory method, this would give you your Cost of Goods Sold for those 15 units. Properly managing inventory can make or break a business, and having insight into your stock through the perpetual inventory method is crucial to success. Regardless of the type of inventory control process you choose, decision-makers know they need the right tools in place so they can manage their inventory effectively. NetSuite offers a suite of native tools for tracking inventory in multiple locations, determining reorder points and managing safety stock and cycle counts. Find the right balance between demand and supply across your entire organisation with the demand planning and distribution requirements planning features. During periods of inflation, a LIFO system may be more appropriate for companies that do not wish to pay as much in taxes, because it will show a higher COGS expense and a lower net income.

In addition, there is the risk that the earnings of a company that is being liquidated can be artificially inflated by the use of LIFO accounting in previous years. Under the perpetual system, managers are able to make the appropriate timing of purchases with a clear knowledge of the number of goods on hand at various locations. Having more accurate tracking of inventory levels also provides a better way of monitoring problems such as theft. At a grocery store using the perpetual inventory system, when products with barcodes are swiped and paid for, the system automatically updates inventory levels in a database. As inventory is stated at price which is close to current market value, this should enhance the relevance of accounting information. LIFO is extensively used in periodic as well as perpetual inventory system.

Based on the LIFO method, the last inventory in is the first inventory sold. In total, the cost of the widgets under the LIFO method is $1,200, or five at $200 and two at $100. Most companies that use LIFO inventory valuations need to maintain large inventories, such as retailers and auto dealerships.

Most companies that use LIFO are those that are forced to maintain a large amount of inventory at all times. By offsetting sales income with their highest purchase prices, they produce less taxable income on paper. There are several disadvantages of using a periodic inventory system. It can be cumbersome and time-consuming, as it requires you to manually count and record your inventory.